Top 8 Paying Apps to Make Real Money from Home Discover the top 8 paying apps to make real money from home in 2025. Earn cash safely through trusted platforms built for...

Aster Explodes in Value After CZ’s $2M Surprise Buy Aster explodes 30% after CZ’s $2M surprise buy, igniting a wave of investor excitement and speculation about how long...

Discover Hedera (HBAR): The Breakthrough Blockchain of 2025 Explore Hedera (HBAR), the breakthrough blockchain of 2025 powering fast, green, and secure transactions...

How to Build and Sell AI Courses Easily in 2025 Learn how to build and sell AI-powered courses easily in 2025 using no-code tools. Turn your skills into income with...

EU Prepares to Launch New Euro Stablecoin by 2026 European banks plan to launch a euro-backed stablecoin by 2026, aiming to modernize payments, rival the Digital Euro...

The Complete Fetch.ai (FET) Growth & Analysis in 2025 Explore Fetch.ai (FET), the leading AI blockchain project driving automation and smart agent innovation...

How to Build a Personal Brand That Earns Online in 2025 Learn how to build a powerful personal brand that earns online in 2025. Discover proven strategies to grow...

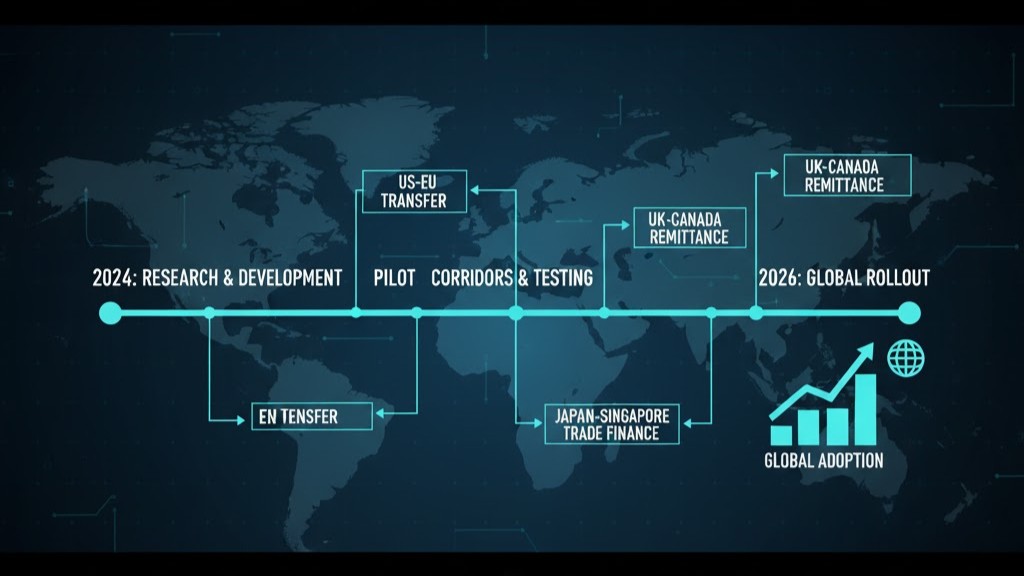

New Crypto Settlement Ledger Coming by Q1 2026 Global central banks prepare to launch a unified crypto settlement ledger by Q1 2026, aiming to revolutionize payments...

The Ultimate Guide to Akash Network and Its AKT Token Explore Akash Network (AKT), the leading decentralized cloud platform powering AI, Web3, and scalable computing...